To every entrepreneur, founder, and business owner: this article is for you.

You’ve poured your heart and soul into building something from nothing. You’ve sacrificed countless hours, taken massive risks, and navigated endless challenges to get to where you are today. Your business isn’t just a company; it’s a living legacy, a testament to your hard work and vision.

But have you ever stopped to consider what would happen if that vision were to suddenly disappear?

It’s an uncomfortable thought, but one of the biggest risks to a business’s survival isn’t a market crash or a new competitor. It’s the unexpected loss of a key person—a founder, a top salesperson, a lead innovator, or a shareholder. When this happens without a plan, the entire business can be at risk of falling apart.

When a Business Loses Its Heartbeat: A Story of Disruption

Across the globe, history is filled with stories of companies that stumbled, or even collapsed, after losing a key individual. The Reliance Industries empire in India, for example, was rocked by a public feud and division after its founder, Dhirubhai Ambani, passed away without a will. This lack of a succession plan led to a bitter, three-year struggle between his sons, ultimately splitting the company in two and causing immense disruption.

These examples teach us a crucial lesson: your hard work is a valuable asset, but it needs a plan for the future. You have to protect the business itself.

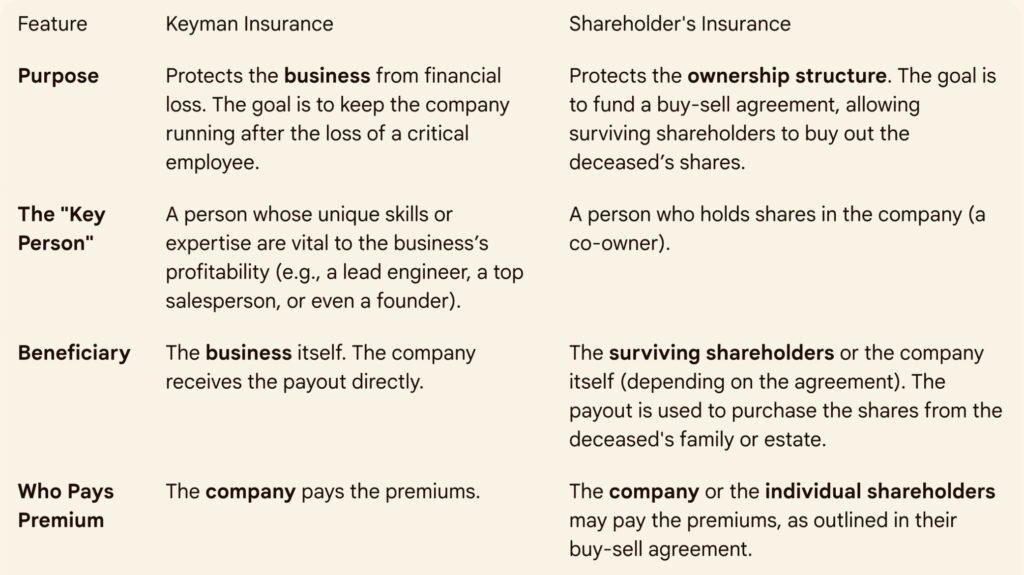

This is where Keyman and Shareholder’s Insurance come in, acting as a crucial safety net.

Keyman vs. Shareholder’s Insurance: Two Different Shields

These two types of insurance are often mentioned together, but they serve two very different, yet equally important, purposes. Think of them as two distinct shields that protect different aspects of your business.

Keyman Insurance is about business continuity—the company gets the money to cover costs like recruiting a replacement, training new staff, or offsetting lost revenue. Shareholder’s Insurance is about ownership continuity—it provides the funds to prevent a deceased shareholder’s family from inheriting shares and potentially disrupting the business.

Beyond the Basics: What Else You Should Know

To truly protect your business, there are a few other things to consider when setting up these plans:

- The Power of the Buy-Sell Agreement: Shareholder’s Insurance works hand-in-hand with a legal document called a buy-sell agreement. This agreement, drafted by a lawyer, outlines the terms for the transfer of shares. The insurance simply provides the necessary funds to make that agreement work. Without this legal document, the insurance payout alone cannot force the sale of shares.

- The “Double Whammy” Strategy: In many cases, a single person can be both a key person and a shareholder. Think of a founder who owns 50% of the company. Their loss would cause both a financial blow to the business and a disruption to its ownership. In this scenario, it is wise to have both types of insurance to cover all bases.

- Tax Considerations: The tax treatment of premiums and payouts can vary based on your business’s structure and local regulations. It is always wise to consult with a financial planner and a tax professional to ensure your policies are set up correctly to minimize tax liabilities.

Your business is your legacy. You’ve worked tirelessly to build it from the ground up. Now, it’s time to put a simple, effective plan in place to protect it for the long run. By proactively thinking about succession and getting the right insurance, you’re not just securing your business—you’re securing your peace of mind.