Five years in this industry and I keep seeing the exact same pattern: people buying insurance a step too late or completely missing their golden chance of getting covered before an illness arrives. Critical illnesses and deaths around us feel like never-ending stories. Yet, the life cycle moves on. Children grow. People get married. They have children of their own, and those children grow. At 40 years of age, I feel like I have almost seen it all.

What differentiates people are those who are proactive and diligent in taking control of their finances and protection, versus those who prefer to live in uncertainty—leaving life to chance with the confidence that life will never hit them hard, until it is too late.

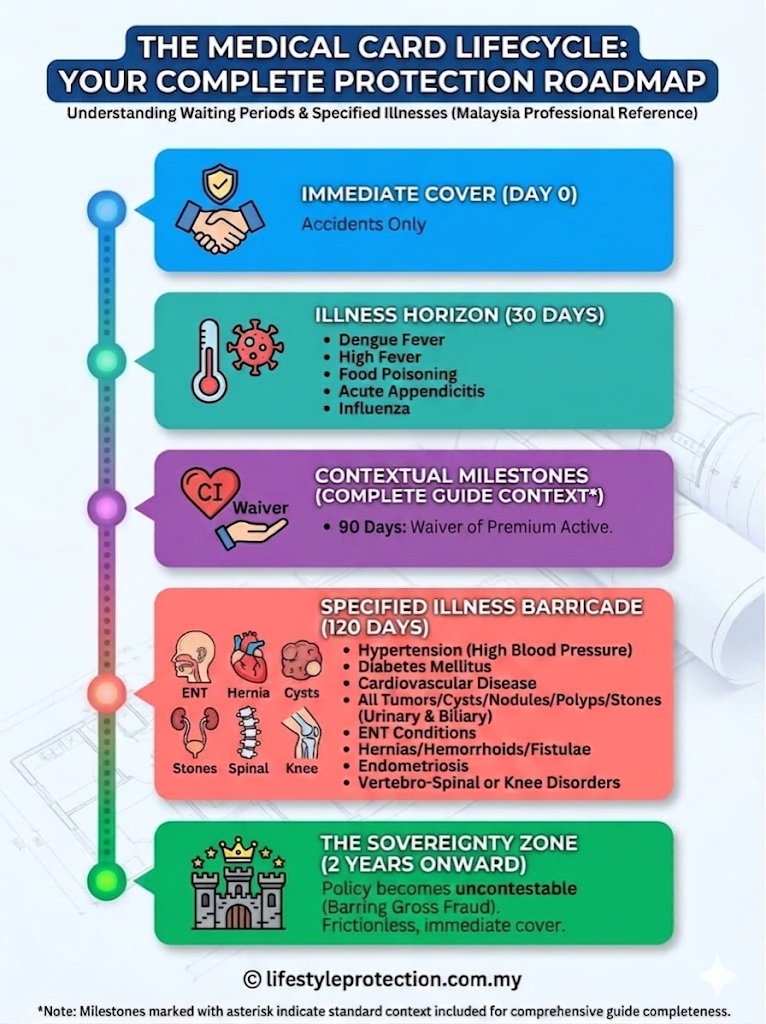

When we are young and healthy, we view ourselves as invincible. But the underwriting system doesn’t operate on optimism; it operates on cold, hard data. If you understand the timeline of how a medical card actually matures, you realize that delaying your application is a massive gamble against time.

The Hard Realities of the Contract

The reason I am talking about this is that I want readers to know that every medical card has its own waiting period and a two-year contestability period. It does not cover pre-existing illnesses. If any early detection is found during your regular GP checkup, it must be disclosed to the insurance company when you are applying for cover. For example, ‘chest pain’, which could lead to heart attack. Let the underwriters know what risk you are carrying, and let them request further medical checkups if needed. They will bear the costs.

If the health risk is high (meaning, you have a very high probability to be admitted to a hospital in the future due to your existing health condition), a premium loading may apply, but at least you get a solid confirmation from the insurance company that anytime you are admitted for surgery, they are ready to cover you. Because if you give the insurance company surprises via hidden illnesses, that is when the cover is withdrawn, and they will refuse to pay for your medical expenses.

The Lifecycle of a Medical Card

To help you visualize what you are actually signing up for, it helps to look at the strict lifecycle of a medical policy:

The Legacy of the “Field Underwriter”

Remember, insurance is a black-and-white contract. Honesty is always the best policy. Insurance agents play a vital role in handling customer due diligence. Once upon a time, insurance agents were called “field underwriters.” We work on the road to meet clients and understand their health risks before passing the application and disclosures to the office underwriters.

Every once in a while, you will find people complaining about insurance companies refusing to pay for their hospital admissions. The reasons are almost always the same: non-disclosure of illnesses prior to buying the medical card.

During that initial two-year contestability period, the insurance company has the legal right to contest and investigate if there is any evidence of early signs or pre-existing illnesses prior to the application. This is why it is always incredibly disappointing to see clients whose medical cards have matured past the two-year mark suddenly decide to cancel their cover. They are walking away right when it has finally protected them—with the contestability clause no longer being an issue.

At that stage, if an illness strikes you, it is going to be immediate cover with no lengthy investigations. (Though, of course, if the treating doctor suddenly sends a report stating you had the condition many years before you applied, that may still trigger an investigation). But if you’re clean, there is nothing to worry about.

So, why do we even need a medical card when it seems so hard to get claims paid? Why do so many people still want to get covered?

I have seen a baby being admitted to the hospital repeatedly almost every month, and the parents have nothing to worry about because the admissions are approved every single time. I have seen a client with ear infection to the point of almost deaf, being treated in a private hospital immediately and discharge the next day. I have also seen a client admitted for cyst on the breast, we went through AIA investigation because the medical card was not yet mature two years, and AIA reimbursed the hospital bill because she has no previous health history. The same goes to another client who diagnosed with sinus, went through investigation because her medical card was not yet 2 years matured, also got her hospital bill reimbursed. I have seen an ex-colleague diagnosed with cancer and didn’t have to pay a single cent because everything was covered by her medical card – it was already past 2 years maturity. There are actually more success and joyful stories than the sad ones.

All I can say is, now that you know these facts—about the waiting period and the contestability period—would you still delay your decision to get a good medical card when you know you are healthy today, or would you rather wait until it is an hour too late to finally decide?

Beyond the Medical Card: Building a True Fortress

Let’s take a step back. A medical card only does one thing: it pays the hospital bill so you don’t have to drain your personal liquidity. It doesn’t replace your active income, it doesn’t buy your groceries, and it doesn’t clear your liabilities while you are recovering at home. True self-stewardship requires a multi-layered defense.

Personally, I have more than just a medical card. I have a personal accident cover that pays a daily income just in case an injury prevents me from working day-to-day. I have critical illness cover because I know the health history within my family and relatives. I have travel insurance because if anything happens overseas, I don’t want to drain a bulk amount of money on international medical expenses—plus, it covers curtailments like sudden floods or cancellation, allowing me to claim refunds for prepaid hotel bills and flights tickets. I even have an MLTA for my home mortgage.

I live by this principle: if I don’t take care of myself, who else will? And if I cannot even take care of myself, how am I going to take care of my loved ones and the people around me?

Taking control of your protection portfolio isn’t about fearing the worst; it is about respecting the life you are actively building. It is about locking in your sovereignty while your health is still an asset, rather than trying to negotiate with an underwriter when it has already become a liability.

Stop leaving your life to chance. Build your fortress while the sun is still shining, so that when the storm eventually arrives, all that is left for you and your family to do is exhale.

Let’s audit your baseline protection together before time makes the choice for you.