Author’s Note: This article is a strategic deep dive into structuring your foundational wealth. If you’ve ever felt the frustration of “lifestyle creep” eating away at your hard-earned income, or if you simply want a structured space to park your active cash where it will be forced to grow, this piece is written specifically for you. Grab a good cup of coffee, and let’s explore how to trap your financial energy and architect an unshakeable baseline for your future. Article updated on 27/3/2026.

If you are reading this, you are likely in a powerful phase of your life. You are generating active income, building your career, scaling a business, or raising a family. You are making good money, but perhaps you’ve noticed a subtle friction: lifestyle creep. As your income grows, expenses tend to expand alongside it, leaving cash sitting idle in low-yield accounts or dissolving into everyday living.

Before you can build a multi-generational fortress, you must first pour a flawless concrete foundation. You need a mechanism that traps your active financial energy, enforces discipline, and automatically compounds your capital over time.

Today, I want to explore a strategic tool designed exactly for this foundational phase: A-Enrich Rezeki. Let’s elevate how we view this Shariah-compliant instrument, moving beyond “basic savings” to look at its profound structural architecture.

1. The “Sprint to Compounding” (Time Leverage)

We are often perfectly willing to commit to a 5- or 9-year installment plan for a vehicle—an asset guaranteed to depreciate. What if you applied that exact same discipline to a guaranteed 20-year runway of wealth compounding?

A-Enrich Rezeki operates on a powerful principle of time leverage through two distinct “sprint” structures:

-

The 5Pay20 Sprint: You deploy capital for just 5 years, and the structure protects and compounds your wealth for a full 20 years. The minimum commitment is highly accessible at RM 12,000 annually (RM 1,000/month).

-

The 10Pay20 Sprint: A steadier marathon where you deploy capital for 10 years, securing a 20-year runway. The minimum commitment is RM 6,000 annually (RM 500/month).

You do not have to pay forever. You do the focused, heavy lifting for a short period, and then you let time and the market do the rest.

2. The Architecture of Your Capital: Understanding the 75/25 Split

In a conscious financial plan, transparency is the foundation of trust. It is important to note that this is not a traditional mutual fund where 100% of your money is exposed to market fluctuations. Instead, A-Enrich Rezeki utilizes a hybrid allocation model designed specifically for capital stability.

When you deploy your annual contribution, it is strategically divided into two distinct “engines”:

-

75% Allocation (The Savings Engine): This majority portion is directed into the Participant’s Savings Fund (PSF). This is the “safe harbor” of your policy. It is from this fund that your massive Maturity, Savings, and Vitality boosters are calculated.

-

25% Allocation (The Growth Engine): The remaining 25% is channeled directly into the Participant’s Investment Fund (PIF). This portion is allocated to purchase units in your chosen global or local Shariah-compliant funds.

This “stability-first” approach ensures that while one part of your money captures market upside, the larger part is anchored in a structure designed to trigger high-value rewards upon maturity.

3. Structural Rewards for Discipline (The Boosters)

A-Enrich Rezeki is engineered with a mathematical reward system designed to incentivize your financial discipline. These are not random bonuses; they are structural injections into your portfolio:

-

The Investment Booster: AIA injects a percentage of your Annual Contribution directly into your portfolio every year (from Year 2 to 19). Depending on your chosen sprint, this scales from 5% up to 30%.

-

The Maturity & Savings Boosters: If you complete your 20-year journey without breaking the structure (by paying on time and refraining from early withdrawals), you receive a Maturity Booster of 200% (for the 5-year sprint) or 400% (for the 10-year sprint) of your Annual Contribution, plus a Savings Booster of 40% or 50%.

-

The Vitality Booster: By maintaining an active lifestyle through AIA Vitality, you can receive an additional boost of up to 200% of your basic annual contribution.

4. The 20-Year Masterclass: A Real-Life Timeline

To truly understand the power of this architecture, let’s look at exactly how these mechanics flow over a 20-year timeline.

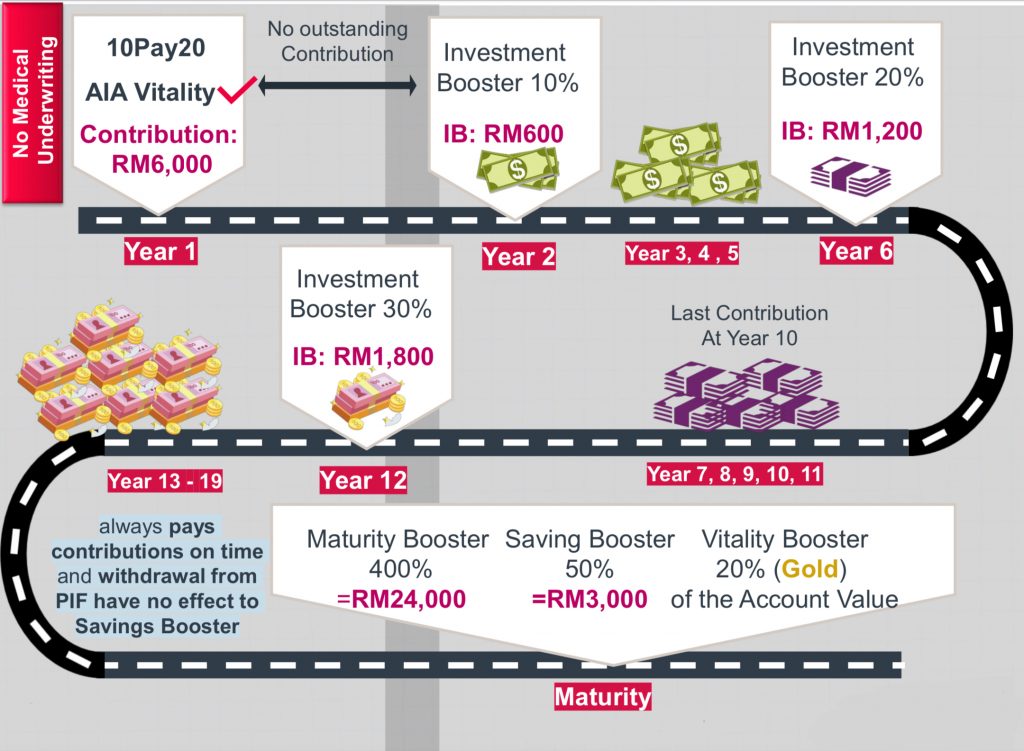

Imagine Sarah, a 30-year-old rising professional. She decides to architect her foundation using the 10Pay20 Sprint, committing RM 500 a month (RM 6,000 annually).

-

The Hustle Years (Age 30–35): Sarah makes her monthly RM 500 deposits. She treats it as a non-negotiable fixed expense. By Year 2, the plan begins rewarding her discipline, injecting a 10% Investment Booster (RM 600) into her account every year.

-

Life Expanding (Age 36–40): Sarah might be buying a home or starting a family. Expenses rise, and the temptation to stop saving is high. But because she is committed to the 10-year sprint, she pushes through. The plan recognizes this consistency. From Year 6 onward, her structural reward doubles to a 20% Investment Booster (RM 1,200) injected annually.

-

The Finish Line (Age 40): Sarah makes her final RM 500 payment. Her total deployed capital is exactly RM 60,000. Her payment term is officially over. But her wealth accumulation is just getting started.

-

The Coasting Phase (Age 41–49): Sarah is now in her peak earning years, focusing fully on her career and family with zero monthly obligations to this plan. Yet, in the background, the plan is now injecting a massive 30% Investment Booster (RM 1,800 annually) straight into her portfolio to continuously buy more units.

-

The Harvest (Age 50): The 20-year mark. Sarah reaches maturity. AIA injects the grand finale: a 400% Maturity Booster (RM 24,000) and a 50% Savings Booster (RM 3,000) directly into her account value.

The Mathematical Reality: Over 20 years, simply by remaining disciplined with her RM 60,000 capital, the plan structurally injected RM 51,000 in guaranteed boosters (RM 24,000 in Investment Boosters + RM 24,000 Maturity Booster + RM 3,000 Savings Booster). And that is before factoring in the actual market growth of the Shariah-compliant funds her capital was invested in. At age 50, she unlocks a massive, fortified lump sum ready to fund her child’s university education or serve as her unshakeable retirement base.

5. The Shariah-Compliant Fortress (Protection & Hibah)

While you accumulate capital, your family’s security remains uncompromised. As a Takaful product, it provides an immediate lump-sum payout in the event of death or Disability.

Crucially, it utilizes Hibah (a conditional gift). Hibah is uncontestable and creditor-proof, ensuring that your wealth flows directly and instantly to your intended loved ones without being trapped in probate. Simultaneously, your wealth grows in alignment with ethical, resilient sectors through Shariah-compliant funds.

6. Architect’s Advice: The “Anti-Procrastination” Anchor for Your DIY Portfolio

If you are managing your own financial planning, you’ve likely experienced the “Liquid Savings Trap.” It is incredibly easy to start an automated transfer into ASB, ASNB, or a high-yield bank account. But because those vehicles are highly liquid, you are constantly faced with the temptation to withdraw from them.

I see this pattern often. When we are suddenly facing too many tasks, expenses, or financial micro-decisions at once, it creates a sense of overwhelm. This causes an energetic withdrawal that leads directly to procrastination—or in this case, abandoning our long-term savings goals for short-term comfort.

Peace must be our priority. We must stop this pattern so we do not lose what is truly important: being a steward to our own financial sovereignty. This is exactly where A-Enrich Rezeki shines as your “Mid-Range Defensive Anchor.” Here is how it fits into a balanced, conscious portfolio:

-

The Liquid Buffer (0-6 Months): Use ASB or bank savings for immediate emergencies only. This is your highly liquid “shallow water” fund.

-

The Disciplined Foundation (A-Enrich Rezeki): This is your “Deep Water” fund. Because the 5-pay or 10-pay structure requires consistent commitment, it effectively “forces” you to save. It acts as a non-negotiable pillar alongside your EPF and PRS, ensuring you don’t accidentally spend your child’s university fees or your retirement base on temporary desires.

-

The Growth Engine (Equities & Legacy): Once your foundation is locked in and your savings habit is “trained” by your A-Enrich Rezeki commitment, you can then graduate into high-leverage assets with the confidence of a seasoned investor. In fact, if you feel you have already mastered this foundational phase and are now looking to architect a multi-million Ringgit, multi-currency fortress for your descendants, I invite you to explore my advanced masterclass: [Link: Beyond Accumulation: The Long-Term Architecture of Generational Wealth with AIA Infinite Heritage].

Securing Your Baseline

True wealth is built by those who have mastered the art of staying the course. If you have struggled with the “easy-in, easy-out” nature of liquid savings, A-Enrich Rezeki provides the necessary structure to protect you from your own impulses. It is a commitment to your future self.

Are you ready to stop “borrowing” from your future and start architecting a foundational wealth that stays put? Let’s connect and map out your accumulation strategy.