Enrich Rezeki is for those who are looking to build their retirement or children’s education fund. The minimum amount of contribution per month is RM 500, equivalent to RM 6,000 per year and up to RM 50,000 per year.

The example in this article is for RM 500/month @ RM 6,000 per year.

How does it work?

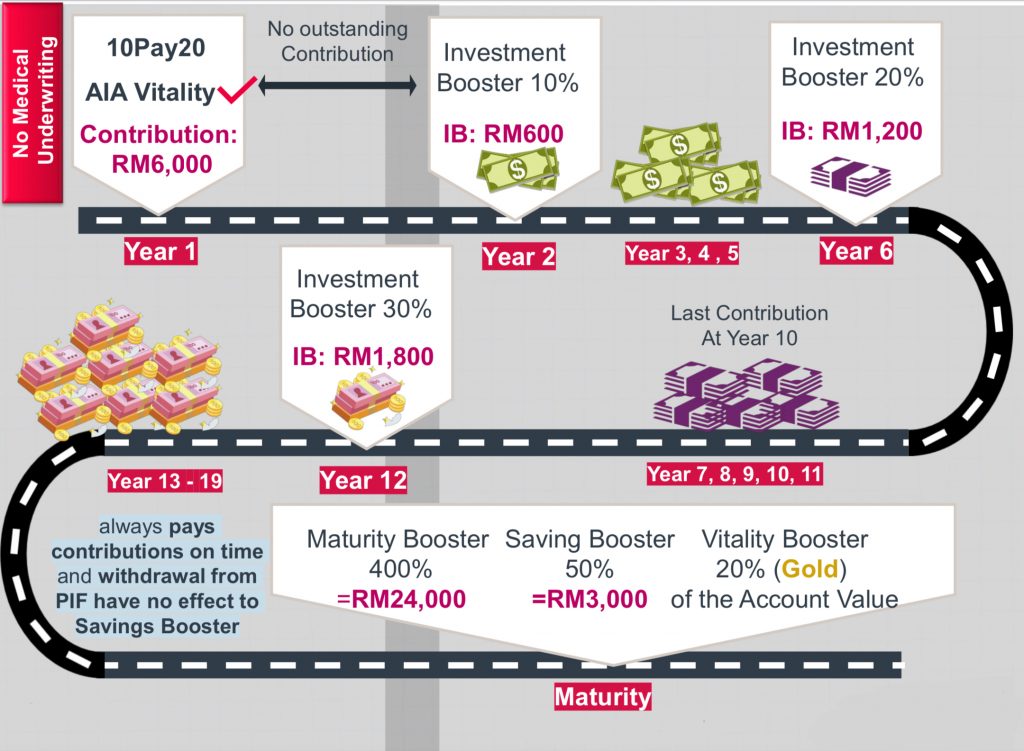

This is a 10pay20 plan, which means, you will have to contribute for the first 10 years and let it grow for the next 10 years until it reaches maturity at the 20th year. For those with no outstanding contributions during the payment term, Enrich Rezeki will reward you with an investment booster of 10% out of your annual contribution (10% x RM 6,000 = RM 600) at the end of the 2nd year, followed by the end of the 3rd, 4th, and 5th year.

The investment booster will increase to 20% (20% x RM 6,000 = RM 1,200) as long as the premium is paid in due time as well as to reward you for your good savings habit. This amount of RM 1,200 will be credited into your account at the end of the 6th, 7th, 8th, 9th, 10th, and 11th years. And remember, your last contribution will be on the 10th year and you have completed your savings instalment plan.

To encourage you to save longer and allow the account value to grow with its compounding interest, Enrich Rezeki will reward you with another 30% investment booster (30% x RM 6,000 = RM 1,800) at the end of the 12th, 13th, 14th year up to your 19th year.

I mean, isn’t it nice to get a passive income credited into your account every year?

When the plan matures on its 20th year, Enrich Rezeki will reward you with a Maturity Booster, 400% times your annual contribution (400% x RM 6,000 = RM 24,000) with an additional Savings Booster, 50% times your annual contribution (50% x RM 6,000 = RM 3,000). And if you are a member of AIA Vitality, by achieving at least Gold Status, you will get an additional 20% boost out of your existing account value.

You would have saved RM 60,000 over 10 years and based on the estimated total maturity benefit, you are looking at growing your money into RM 86,701.05 in 20 years (this estimation is based on 5% fund returns).

Where will my money be invested?

Out of RM 500 of your monthly contribution, 75% will go into savings funds – where you will enjoy the investment booster and maturity rewards, while another 25% (RM125) will go into investment. Usually, the investment in Takaful Plans goes to the local market only. However, with Enrich Rezeki, you will get the chance to invest in the global market.

The global market refers to international giant companies which adhere to Shariah investment guidelines. These companies are in the technology, consumer goods, healthcare, and financial sectors, and I would call them pandemic-proof industries.

What if I pass away before the plan matures?

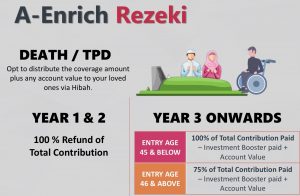

If you pass within the first and second year, your beneficiary will receive 100% refund of total contribution. For the third year onwards, this will also include your investment booster and account value from your investment-linked portion. Please take note that 75% of total contribution paid will be refunded to those with entry age 45 and above but bear in mind, that your investment boosters and account value may have already surpassed the total contribution you paid.

Safe to say, when we are saving our money, the best place to save is a plan which can safeguard your initial capitals. For me, you may reap the benefit of Takaful’s most important criteria – that the Hibah is uncontestable and creditor-proof so you can ensure that the money you save will go to the right person.

Can I opt for shorter payment term?

Enrich Rezeki has two options for its payment term. For 10 years payment term, the minimum contribution per month is RM 500 (or RM 6000 annually). For those who would like to invest more in a shorter time – 5 years payment term, the minimum contribution per month is RM 1,000 (or RM 12,000 annually).

You see, we are willing to commit to 5 – 9 years instalment plan for our cars, although we know that the price of the car will depreciate over the years. Why not commit to our retirement plans, too? Regardless where you decide to save your money, as long as the benefit and return rates are higher than the inflation rate, then you are protecting your money’s buying power for the future.

On a final note

Different people has different financial goals and you may want to have a further discussion on your financial planning with our life planner. Feel free to reach out to us via the Contact Us section below.